The Fed held rates steady at 3.50–3.75% yesterday, but that's not really the news. What matters is they stripped out the language about future cuts and left the door open for another hike. Your equipment dealer already got the memo—financing on that new zero-turn went up again last week.

Landscaping companies across the midwest are scrambling right now. Not because of the Fed announcement itself, but because their pricing structure from March is already outdated. Operators who locked in spring contracts at old margins are getting squeezed between higher financing costs and labor pressure they didn't build into their numbers.

The immediate operational squeeze

That truck loan that would've been $580/month in January is now $640. Equipment financing jumped from around 7% to 9.5% for most landscapers. Working capital lines went from 8% to nearly 11%. These don't sound like huge numbers until you remember you're running 12–15% net margins. A 2% increase in financing costs eats a massive chunk of what's left.

The bigger problem is most landscaping operations built their 2026 pricing on assumptions that rates would drop by summer. They priced maintenance contracts in February expecting cheaper money by June. Now they're locked into those prices through October while costs keep climbing.

The seasonal labor situation compounds it. You need to float payroll for 8–12 crew members from March through November, but commercial clients pay net-30 or net-45. That cash flow gap used to cost around $1,800 a month on a working capital line. Now it's $2,400. Over a seven-month season, that's an extra $4,200 off the bottom line before you've even talked about anything else.

What's frustrating to watch is companies still using last year's pricing models. They haven't adjusted hourly rates, haven't updated equipment replacement calculations, and definitely haven't changed payment terms. They're essentially subsidizing their customers' lawns with their own margins.

Repricing reality: the moves that actually work

Across-the-board price increases are lazy and customers see through them immediately. The operators doing this well are getting surgical about where and how they adjust.

Never miss a job detail again.

Yardyly helps you plan, confirm, and manage every landscaping project seamlessly.

- Centralized project scheduling

- Automated client updates

- Crew and resource management

No credit card required

Start with commercial contracts. Most have escalation clauses that nobody ever uses. Pull them out. If material or financing costs increase more than 5%, you can typically trigger a mid-season adjustment. One Ohio company executed this across 22 commercial properties recently and recovered around $3,400 monthly in margin.

Residential maintenance is trickier—you can't just raise prices mid-season. But you can adjust the service mix. That weekly mowing at $65? Keep it there, but unbundle edging and blowing as $15 add-ons each. Customers who want full service pay $95 total. You're not hitting them with a 46% increase, you're giving them a choice. In practice, about 70% keep the full service, 20% drop to mowing only, and 10% leave. Revenue per route goes up because you're doing less work for the ones who scaled back.

Payment terms move the needle more than most people expect. Push commercial clients from net-45 to net-30. Offer residential customers a 3% discount for same-day payment. Those shifts alone can free up $15,000–$25,000 in working capital for a mid-sized operation. At current rates, that's roughly $200 saved monthly in carrying costs.

The equipment financing game has changed too. Stop financing everything at 60 months. Buy used for anything that isn't customer-facing. A three-year-old commercial mower at $8,000 cash beats a new $15,000 unit at 9.5%. You save close to $7,800 in interest over the loan term, and you can sell it for around $4,000 in two years when the financed one has dropped to $6,000.

Crew decisions when money costs more

Higher rates mean your hiring triggers need recalibration. That standard rule about adding crew at 85% capacity? Move it to 92%. The carrying cost of an underutilized employee went up by roughly $180 per month when you account for working capital needed to float payroll.

Rather than hiring full crews, split the approach. Bring on one lead operator and supplement with day labor through apps like Wonolo or Instawork. Fixed labor costs drop by around 40% while you keep flexibility. A full four-person crew runs about $8,400 weekly. One lead plus on-demand labor covers the same work for around $5,200.

Overtime math changed too. At current rates, financing overtime adds about 0.75% monthly. But a new hire means training costs, workers comp deposits, and equipment. The breakeven shifted from 8 hours of overtime weekly to roughly 11 hours. Until your crew is consistently hitting 51-hour weeks, overtime is still cheaper than expansion.

Your KPI triggers for hiring decisions need updating across the board. Revenue per crew member, jobs per day, drive time percentage—all those thresholds shift when capital costs more. A crew generating $12,000 weekly made sense at 6% rates. At 9%, you need closer to $13,500 to hit the same profit margin.

Equipment moves that preserve capital

Cancel the new truck order. The difference between a 2024 F-350 at $68,000 and a 2021 at $45,000 is massive at 9.5% financing. You're looking at $28,000 in interest on the new one versus $17,000 on the used. That $11,000 gap buys a lot of maintenance.

What's actually working for equipment strategy right now:

Lease-backs on existing equipment. Sell owned trucks and mowers to a leasing company, then lease them back. You free up $40,000–$80,000 in capital immediately while keeping the same equipment. Use it to pay down higher-interest debt or fund operations without drawing on credit lines.

Share agreements with non-competing contractors. Partner with a hardscaping company. You use their skid steer two days a week, they use your aerator in fall. Both sides avoid financing specialized equipment that sits idle 70% of the time. Legal docs cost maybe $1,500 and save $15,000+ annually in financing costs.

Tiered equipment quality. Crew leaders get newer, reliable trucks. Support crews run older units. Customer-facing equipment stays sharp, back-end stuff just needs to run. This cuts equipment financing needs by around 35% without touching service quality.

Stop financing small equipment and attachments outright. A $3,000 aerator at 9.5% for 36 months costs $520 in interest. Buy it used for $1,800 or rent it at $200/day when needed. Most landscapers use aerators maybe 20 days a year—that's $4,000 in rental against $3,520 to finance new. Rent wins.

When considering lease-backs, prioritize deals that free up capital without adding onerous maintenance obligations back onto your balance sheet.

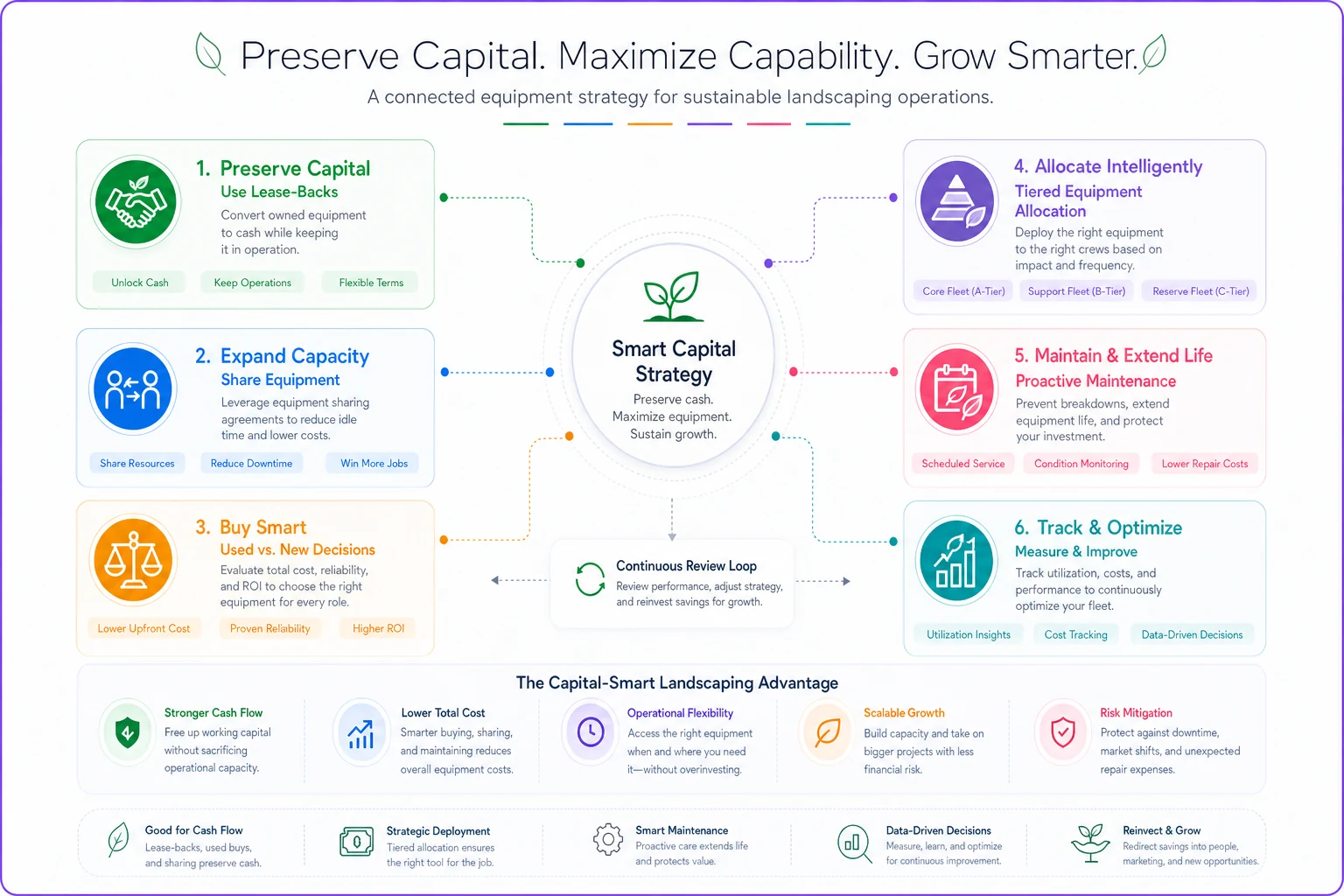

Here's a quick visual workflow to consider for preserving capital through equipment decisions.

Stop financing small equipment and attachments outright. A $3,000 aerator at 9.5% for 36 months costs $520 in interest. Buy it used for $1,800 or rent it at $200/day when needed. Most landscapers use aerators maybe 20 days a year—that's $4,000 in rental against $3,520 to finance new. Rent wins.

Cash flow adjustments that actually matter

Your collection timeline drives everything now. Every day a payment sits outstanding costs real money. At current working capital rates, $10,000 in receivables costs you $3 daily in interest. Across 40 commercial accounts averaging 38 days to pay, that's roughly $4,500 monthly just waiting on checks.

Set up ACH autopay wherever possible. Offer a 2% discount to make it happen. You'll give up some margin but gain predictable cash flow, and the interest savings usually offset the discount within 60 days. You also eliminate the time drain of collections calls.

Progress billing on larger projects is no longer optional. Don't wait for completion on a $15,000 installation. Bill 40% upfront, 30% at midpoint, 30% at the end. Your cash float drops from $15,000 for 45 days to $4,500 for 15 days. Interest savings around $280 per project—adds up fast across a full season.

Net-60 terms should be dead to you. If a customer demands them, price it in—add 4% to cover carrying costs. Most will find net-30 suddenly workable. The ones who don't are at least paying for the privilege of holding your money.

Operational software matters more when capital is expensive. Manual billing delays, missed charges, and data entry errors all stretch your cash conversion cycle. Every day you recover through automation drops straight to the bottom line. Clean operational data also lets you see clearly which services, routes, and customers actually generate positive cash flow after financing costs—something a lot of operators genuinely don't know.

Material and inventory strategies

Stop stockpiling. That bulk fertilizer pallet might be 8% cheaper, but financing inventory at 11% for three months erases the discount. Order weekly based on confirmed jobs. You'll pay slightly more per bag and save meaningfully on carrying costs.

Push suppliers for net-45 or net-60 terms. They have better financing access than you and they want your business. Let them carry the inventory cost. If they won't move, find ones who understand the current environment.

For high-value materials—lighting fixtures, pavers, specialty plants—look at consignment agreements. Suppliers maintain ownership, you avoid financing inventory you haven't installed yet. This can free up $20,000–$40,000 in working capital for an established operation.

Chemical purchasing needs a rethink too. Those 55-gallon drums look economical but lock up cash for months. Switch to smaller quantities with more frequent delivery. Per-gallon cost goes up maybe 12%, but you cut 60–90 days of carrying cost at 11% interest. Net result is actually around 4% in savings.

The pricing conversation that works

Don't surprise existing customers. Send a straightforward email explaining what's happening. Skip the political angle. Just state it plainly: equipment financing costs increased 35% this year, and you're adjusting service structure to maintain quality while managing those costs.

Give them options, not an ultimatum.

-

Full service at the new price

-

Reduced service at current price

-

A prepayment discount for the season

Most operators who've done this right see about 60% take the full-service increase, 25% prepay for the discount, and 15% reduce scope. You hold 97% of revenue while actually improving cash flow.

For new proposals, break out financing costs explicitly.

| Item | Amount |

|---|---|

| Service cost | $180 |

| Equipment allocation | $22 |

| Financing charge | $8 |

| Total | $210 |

Customers who see the breakdown negotiate less aggressively than those who just see a number that's higher than last year.

With commercial clients, skip the maintenance manager and get to the CFO. They understand rate environment impacts. Explain how their payment terms directly affect your financing needs. Most will work with you on terms when you're direct about it.

What happens next

The Fed's signaling points to rates staying elevated through 2026, possibly into 2027. Equipment dealers are already pricing in another 0.5% bump. Banks are tightening lending standards for seasonal businesses. This isn't a temporary squeeze—it's the operating environment for at least the next 18 months.

Operators who don't adjust will bleed margin until they can't sustain it. Consolidation will accelerate as smaller companies struggle with the financing burden. Larger operators with better credit access will pick up distressed competitors at discounts.

Prepared operators will find opportunities in that. Competitors who can't adapt will exit markets. Customers will gravitate toward providers who navigate the environment professionally. The companies restructuring now will take market share from the ones waiting for rates to magically drop.

Your moves over the next 30 days need to be deliberate. Reprice with intelligence, not desperation. Restructure equipment plans around capital preservation. Adjust hiring thresholds to reflect what money actually costs. And get aggressive about cash flow because every day matters when borrowing is expensive.

The landscaping companies still standing in 12 months won't necessarily have the newest equipment or the biggest crews. They'll be the ones who understood that when rates hit these levels, the entire operational playbook needed a rewrite. The math changed in June—make sure your business model changed with it.

Ready to grow your landscaping business?

Join 2,000+ landscaping pros using Yardyly to save time, reduce task chaos, and deliver outstanding client results.